Your engine just died. The mechanic gives you a number that makes your stomach drop. You check your credit score — and it’s nowhere near what a bank wants to see. That feeling? Millions of Americans know it well. Here’s the thing though: a rough credit history doesn’t mean you’re out of options. Engine financing no credit check programs exist exactly for this moment. They’re fast, they’re accessible, and they don’t punish you for your past.

This guide covers everything — how these programs work, who qualifies, what it costs, and how you can get approved today without a single hard inquiry hitting your credit file.

Engine Financing with No Credit Check Required

Most people assume financing always means a bank pulling your credit report and judging every late payment from the last seven years. That’s not how no credit check engine replacement financing works. These programs skip the traditional credit bureau route entirely. Instead, they look at your current income, your employment status, and your ability to make consistent payments going forward.

There are two types of credit checks — hard and soft. A hard inquiry shows up on your credit report and can drop your score by several points. A soft credit check auto parts review, on the other hand, leaves zero trace. Many engine financing no credit check lenders use alternative credit verification methods — or skip the bureau check altogether — so your score stays exactly where it is when you apply.

| Credit Check Type | Impact on Credit Score | Visible to Lenders | Used In |

|---|---|---|---|

| Hard Inquiry | Yes — can drop 5–10 points | Yes, for 2 years | Banks, traditional auto loans |

| Soft Inquiry | None | No | Most no-credit-check financing programs |

| No Bureau Check | None | No | Alternative credit data approval programs |

No Credit Check Engine Financing — Here’s How It Works

Honestly, this surprised me when I first looked into it. The process is far simpler than applying for a personal loan. You fill out a short online engine financing application — usually takes about five minutes. The lender reviews your income and basic personal details. You get a decision fast, often the same day. Then you pick your engine, confirm your installment plan for engine replacement, and the part ships directly to your mechanic or home. No mountains of paperwork. No waiting a week for a callback.

How to Finance a Replacement Engine Without a Hard Inquiry

Here’s what most people miss. They think “financing” automatically means a bank dragging their credit history into the spotlight. It doesn’t. No hard credit pull engine financing programs exist because specialized lenders have figured out a smarter way to evaluate borrowers. They look at income verification, employment history, and bank account activity — not your FICO number. Think of it this way: a traditional loan is like being judged for a job based only on one test score. These alternative lenders actually interview you as a whole person.

Alternative credit verification methods are now widely accepted in the auto parts financing space. Programs from lenders like Snap Finance engine funding, PayTomorrow engine financing, and American First Finance auto repair all use this model. They aren’t taking a wild risk — they’ve built underwriting systems that assess real repayment ability. According to the Consumer Financial Protection Bureau, over 45 million Americans are “credit invisible,” meaning they have no score at all. These programs were built to serve that exact group.

Get Approved for Engine Financing Regardless of Your Credit Score

Bad credit doesn’t disqualify you. That’s the short answer. Bad credit engine financing programs are specifically designed for people whose scores don’t reflect their current financial reality. Maybe you went through a divorce. Maybe medical bills piled up. Maybe you were young and made mistakes. None of that automatically blocks you from engine financing without credit inquiry approval today.

Financing all credit types is literally the selling point of these programs. Lenders operating in this space — including Synchrony engine financing and NAPA EasyPay engine repair — understand that a low credit score auto repair loan applicant isn’t necessarily a risky one. Someone with a 520 score who’s been steadily employed for two years and earns $3,000 a month is a far safer bet than someone with a 680 score and irregular income. The old system penalized the former. These new programs reward the reality.

“Your credit score is a snapshot of your past — not a prediction of your future.” — This is the philosophy behind no credit needed financing programs, and it’s why they’ve grown significantly in the last decade.

Bad Credit? You Can Still Finance a Remanufactured Engine

Remanufactured engine financing is one of the best-kept secrets in the auto repair world. A remanufactured engine isn’t a used engine with a fresh coat of paint. It’s a completely rebuilt unit — disassembled to its core components, machined back to factory specs, and reassembled with new parts where needed. The result is an engine that performs like new but costs significantly less. For someone dealing with imperfect credit auto financing, this is the sweet spot.

Cost comparison matters here. A brand-new engine for a common vehicle like a Ford F-150 can run $4,000–$7,000 or more. A remanufactured engine for the same truck often costs $1,500–$3,500, depending on the make and supplier. Most rebuilt engine no credit check financing programs cover remanufactured units and include a warranty — typically 12 months or 12,000 miles at minimum. That warranty piece is big. You’re not just getting a cheaper engine. You’re getting a protected one.

| Engine Type | Average Cost | Warranty Included | Eligible for No-Credit Financing |

|---|---|---|---|

| Brand New OEM Engine | $4,000–$9,000 | Yes (manufacturer) | Sometimes |

| Remanufactured Engine | $1,500–$3,500 | Usually yes | Yes |

| Rebuilt Engine | $1,000–$2,500 | Varies | Yes |

| Used Engine | $500–$1,500 | Rarely | Yes |

Engine replacement bad credit USA programs are widely available for all these engine types — but remanufactured units tend to be the most popular choice because the value-to-quality ratio is genuinely hard to beat.

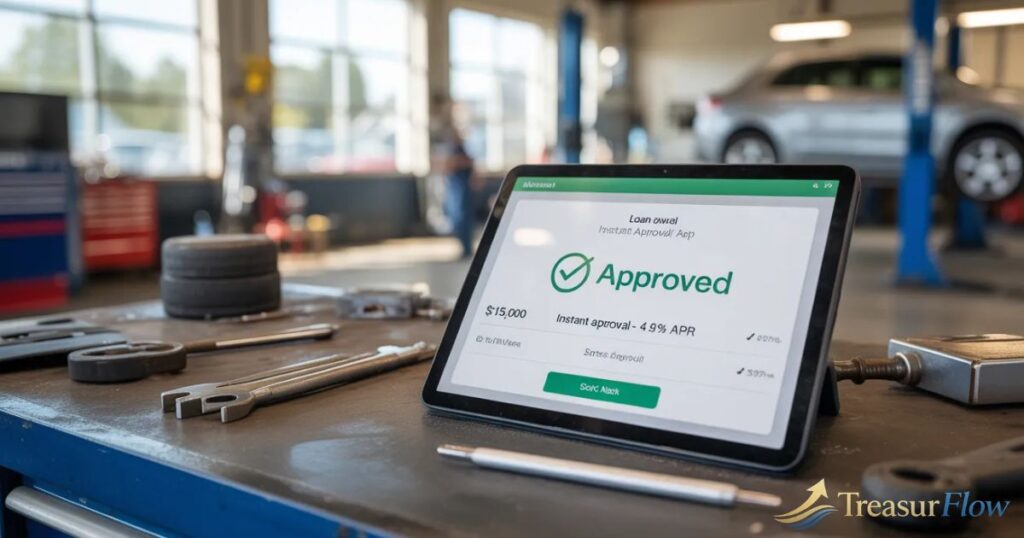

Same-Day Approval: Engine Financing Without the Credit Hassle

Time matters when your car is sitting dead in a parking lot. Same-day financing approval isn’t just a marketing line — it’s a real operational advantage these lenders have built. Traditional bank applications involve credit committees, underwriting queues, and processing delays that can stretch across days or weeks. A pre-approval engine loan through a no-credit-check program can land in your inbox within hours of applying.

Here’s a real-world scenario worth thinking about. It’s Monday morning. Your engine blows on the way to work. You can’t afford to miss shifts. You apply online during your lunch break. By 3 PM, you’re approved. Your replacement engine financing is locked in, payment plan confirmed, and the engine ships within 24–48 hours. That’s the actual timeline these programs are built for. Can’t afford engine replacement anymore isn’t the full story — because now there’s a fast, credit-friendly path forward.

No Credit Check Financing Available for Engines and Transmissions

Not everyone realizes this, but transmission financing no credit check works through the exact same programs. Transmissions fail. Sometimes they go right after the engine does — or instead of it. Replacing a transmission can cost $1,800–$3,500 for a remanufactured unit, and up to $5,000+ for a new one. That’s not small money. Remanufactured transmission financing through no-credit-check lenders means you don’t have to choose between fixing your car and paying rent.

Auto parts financing no credit programs often extend beyond just engines and transmissions too. Some lenders cover transfer cases, differentials, and other major drivetrain components. The engine and transmission loan is bundled into one application, one payment plan, and one approval process. No separate applications. No second hard pull. Drivetrain replacement loan coverage through a single lender keeps things clean and simple — which is exactly what you want when you’re already dealing with a breakdown.

Why Choose No Credit Check Engine Financing Over Traditional Loans

Banks and credit unions weren’t designed for emergency auto parts purchases. That’s not a criticism — it’s just reality. A traditional personal loan for engine repair requires good credit, documentation, processing time, and often collateral. A bank loan vs engine financing comparison makes the gap obvious. Credit score not required programs move faster, serve more people, and focus on the actual repair — not your financial history.

Here’s what that looks like side by side:

| Factor | Traditional Bank Loan | No Credit Check Engine Financing |

|---|---|---|

| Credit Check | Hard pull required | Soft pull or none |

| Minimum Credit Score | Usually 620–680+ | Not required |

| Approval Speed | 3–10 business days | Same day |

| Application Method | In-person or lengthy online form | 5-minute online engine financing application |

| Impact on Credit Score | Yes | No |

| Covers Engine/Parts Directly | Rarely | Yes |

| Flexible Payment Options | Limited | Yes — weekly, bi-weekly, monthly |

No credit check auto loan alternative programs also tend to offer lease-to-own engine financing options. That means you can get the engine installed now, make payments over time, and own it outright at the end of the term. Lease-to-own auto repair is becoming increasingly popular for exactly this reason — it’s accessible, predictable, and doesn’t require perfect credit to access.

Flexible Payment Plans for Engine Replacement — No Hard Pull

Nobody wants to hand over $2,500 upfront for an engine when the car breaking down already wiped out your emergency fund. Engine replacement payment plan options through no-credit-check lenders are built around real budgets. You’ll typically see weekly, bi-weekly, or monthly payment structures — and many programs offer terms ranging from 3 months to 18 months depending on the loan amount and your income profile.

No down payment engine financing is available through several lenders, though some programs ask for a modest upfront amount. The key word is flexible. Flexible engine loan terms mean you aren’t locked into a rigid schedule that doesn’t match how you actually get paid. A crate engine payment plan or engine rebuild financing setup that aligns with your paycheck cycle makes repayment genuinely manageable — not a monthly panic. No credit pull payment plan options protect your score throughout the entire repayment period, not just at application.

Who Qualifies for No Credit Check Engine Financing?

The qualification bar is lower than most people expect. That’s intentional. Engine financing eligibility is designed to be broad because the whole point is serving people traditional lenders turn away. Most programs require a few basic things: you need to be at least 18 years old, a U.S. resident, and have some form of verifiable income. Employment income is the most common — but self-employment income, benefits, and even gig work often count too.

Qualify for engine loan no credit programs typically means meeting these core criteria:

- Age 18 or older with a valid government-issued ID

- Active U.S. bank account (checking accounts are standard)

- Proof of regular income — pay stubs, bank statements, or tax returns

- U.S. residency (most programs serve all 50 states)

- Vehicle identification number (VIN) for engine compatibility matching

Co-signer engine loan options exist for applicants who fall just short of the income threshold. A co-signer with stable income can strengthen the application significantly. Secured engine financing option programs also exist — where you use a paid-off vehicle as collateral — though most no-credit-check programs don’t require this. The no credit history engine purchase path is very much available here. You don’t need a credit file at all — just income and identity verification.

Frequently Asked Questions About Engine Financing with No Credit Check

Can you finance a used engine with bad credit? Yes. Used engine financing bad credit is one of the most common use cases for these programs. Used engines are often the most affordable option, and no-credit-check lenders regularly finance them — especially when the engine comes with a short warranty.

Does financing an engine hurt credit? It depends on the lender. Programs using soft pulls or no bureau credit check methods don’t affect your score at all. Always ask upfront whether the lender uses a hard or soft inquiry before applying.

How to get engine financing with bad credit? Apply through a specialty lender like Snap Finance engine, PayTomorrow engine financing, or American First Finance auto repair. Have your income documentation ready. The process is mostly online and takes about five minutes.

What credit score is needed for engine financing? With no-credit-check programs — none. Credit score not required is a genuine feature, not a gimmick. Income and identity verification are what matter.

How long does engine financing approval take? Most applicants receive same-day financing approval. Some programs return decisions within 15–30 minutes of a completed application.

Is engine replacement financing available in my state? Most major providers cover all 50 U.S. states. Confirm during your application, but availability is broad across the country.

What’s the difference between buy now pay later engine options and installment loans? Buy now pay later engine programs let you get the part immediately and split payments over a short window — often 4 payments over 6 weeks. Installment plans run longer, usually 3–18 months, with lower individual payments. Both fall under the engine financing no credit check umbrella.

Can I get engine financing after bankruptcy? Yes. Engine loan after bankruptcy is possible because these programs assess your current ability to pay — not your past filing history. Many applicants in this situation get approved without issue.

| Question | Short Answer |

|---|---|

| Can you finance a used engine? | Yes |

| Does it hurt your credit score? | No (with soft/no pull programs) |

| What credit score do you need? | None required |

| How fast is approval? | Same day — sometimes minutes |

| Does bankruptcy disqualify you? | No |

| Is it available in all 50 states? | Yes, for most lenders |

Get Back on the Road Today — Apply for Engine Financing in Minutes

Auto engine repair financing no credit needed exists. It works. And it’s available right now, regardless of what your credit report says. The programs covered in this guide — from in-house engine financing to third-party lenders like Snap Finance engine and PayTomorrow engine financing — have helped hundreds of thousands of Americans get their vehicles back on the road without a hard inquiry, without a perfect credit score, and without waiting days for a decision.

Your car broke down. That’s stressful enough. The financing part doesn’t have to add to it. A five-minute online engine financing application is all it takes to start. Engine financing no credit check approval can come through the same day. Your payment plan activates. Your engine ships. And you get back to your life. Don’t let a dead engine keep you parked — get approved engine loan options are waiting for you right now. Apply today and get moving again.

Used Engine Financing No Credit Check (Popular Buyer Choice)

Many users searching for engine financing are not looking for brand-new engines. Instead, they want a more affordable option, which is why used engine financing no credit check has become one of the most common search intents.

Used engines are typically sourced from vehicles that were damaged in accidents but still have fully functional engines. Because of this, they cost significantly less than new or remanufactured engines, making them easier to finance even through no credit check programs.

Most lenders that offer engine financing without credit checks also support used engines because:

- The loan amount is smaller

- Approval risk is lower

- Repayment terms are shorter and more flexible

In most cases, approval is based on income stability rather than credit score, which allows applicants with bad credit or no credit history to still qualify.

If you are searching for used engine financing no credit check near me, the process usually works online. The lender approves you digitally and then ships the engine directly to your mechanic anywhere in the United States.

Car Engine Financing No Credit Check Options

If your search is specifically about car engine financing no credit check, you are not limited to a single solution. These financing programs are designed for all types of passenger vehicles including sedans, SUVs, and trucks.

Instead of relying on banks, these programs use alternative approval methods such as:

- Income verification

- Employment history

- Bank account cash flow analysis

This makes it possible to finance a car engine even if your credit score is low or nonexistent.

The key benefit is flexibility. You can choose:

- Used engines (lower cost, easier approval)

- Remanufactured engines (better quality, longer warranty)

- Payment plans aligned with weekly or monthly income

For most applicants, approval happens the same day, and the engine is shipped directly to a certified repair shop for installation.

Rent to Own Engine Financing (Flexible Ownership Model)

Another growing option is rent to own engine financing, which works differently from traditional loans.

Instead of paying the full amount upfront or taking a bank loan, you make small scheduled payments until you fully own the engine.

This model is useful for people who:

- Do not qualify for traditional loans

- Want lower upfront costs

- Prefer predictable payments over time

In most rent-to-own engine programs:

- You get the engine installed immediately

- You make weekly or monthly payments

- Ownership transfers after final payment

Compared to standard financing, this option is more flexible but may cost slightly more over time due to extended payment terms and service fees.

New Engine Financing vs Used Engine Financing

When choosing between new engine financing and used engine financing, the decision usually comes down to cost versus reliability.

A new engine offers:

- Maximum lifespan

- Full manufacturer warranty

- Higher cost and stricter approval requirements

A used engine offers:

- Lower upfront cost

- Easier approval under bad credit engine financing programs

- Faster availability

For most applicants searching finance a new engine or asking can you finance a new engine, lenders do allow it, but approval is more common for remanufactured or used engines because the loan amounts are smaller and risk is lower.

If your priority is affordability and fast approval, used or remanufactured engines are usually the better choice. If long-term reliability matters more, new engines are worth considering if you qualify.

Loan for Engine Replacement (What Most People Miss)

A loan for engine replacement is often confused with traditional auto loans, but they are not the same.

Standard banks rarely approve engine-only financing because:

- The vehicle may already be damaged

- Loan value is too specific

- Risk assessment is stricter

That is why no credit check engine financing programs exist — they focus only on the engine replacement cost, not the entire vehicle value.

These loans are typically:

- Fast approval (minutes to same day)

- Flexible repayment plans

- Available for both used and new engines

If your vehicle engine has failed, this type of financing is designed specifically for that situation.

Engine Failure on Financed Car (Important Scenario)

If you experience engine failure on a financed car, you are still responsible for your original car loan even if the engine stops working.

This creates a double burden:

- Ongoing car payments

- Unexpected engine repair cost

In this case, many users choose engine financing instead of paying upfront repair costs. It allows them to fix the vehicle and continue using it while spreading the cost over time.

Some lenders even approve financing for vehicles that are still under existing auto loans, depending on income and repayment ability.

FAQs

Can I finance engine replacement costs?

Yes, most no credit check programs allow full engine replacement financing including parts and labor.

Can you finance a new engine?

Yes, but approval is easier for used or remanufactured engines due to lower cost.

Is rent-to-own engine financing available?

Yes, some providers offer rent-to-own plans with weekly or monthly payments until ownership is complete.

What is a loan for engine replacement?

It is a specialized financing option that covers only the engine repair or replacement cost, not the full vehicle.

Sources and References: Consumer Financial Protection Bureau — Credit Invisible Report | Federal Reserve — Report on the Economic Well-Being of U.S. Households | Experian — What Is a Hard Inquiry? | NAPA Auto Parts EasyPay Financing | Snap Finance

Ideas to Help You Think Smarter About Money.