Everything American Business Owners Need to Know Before Offering Financing In-House — Including What Most Guides Won’t Tell You

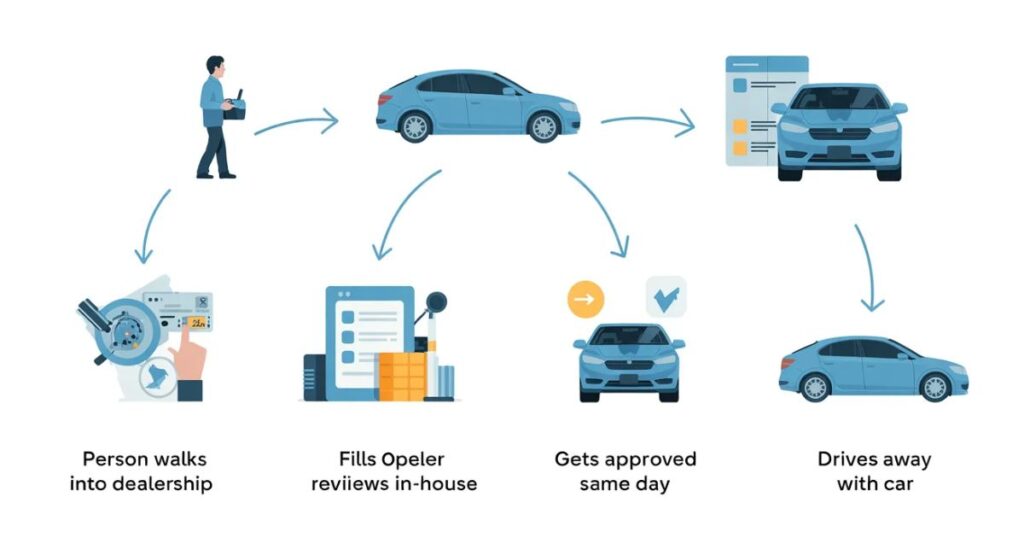

If you’ve ever watched a customer walk out empty-handed because they couldn’t pay the full price upfront, you already understand why in-house financing exists. It’s not a complicated concept. You sell something. The customer can’t pay all at once. So you become the lender. Simple — but the details matter enormously.

According to a 2024 Federal Reserve report, nearly 40% of American adults couldn’t cover an unexpected $400 expense without borrowing. That’s your customer base. A huge chunk of people who want what you’re selling genuinely can’t buy it without a payment plan. In-house financing pros and cons sit right at the center of that reality.

This guide covers everything — the revenue upside, the default dangers, the compliance traps, and the technology that makes it all manageable. Whether you run a used car lot in Texas, a dental practice in Ohio, or a furniture store in Florida, this breakdown applies directly to you.

7 Proven Pros of In-House Financing That Boost Revenue and Customer Loyalty

Here’s what most business owners don’t realize when they first consider in-house financing: it’s not just a payment tool. Done right, it’s a complete customer relationship strategy. When you finance the deal, you own the relationship from sale to final payment. That changes everything.

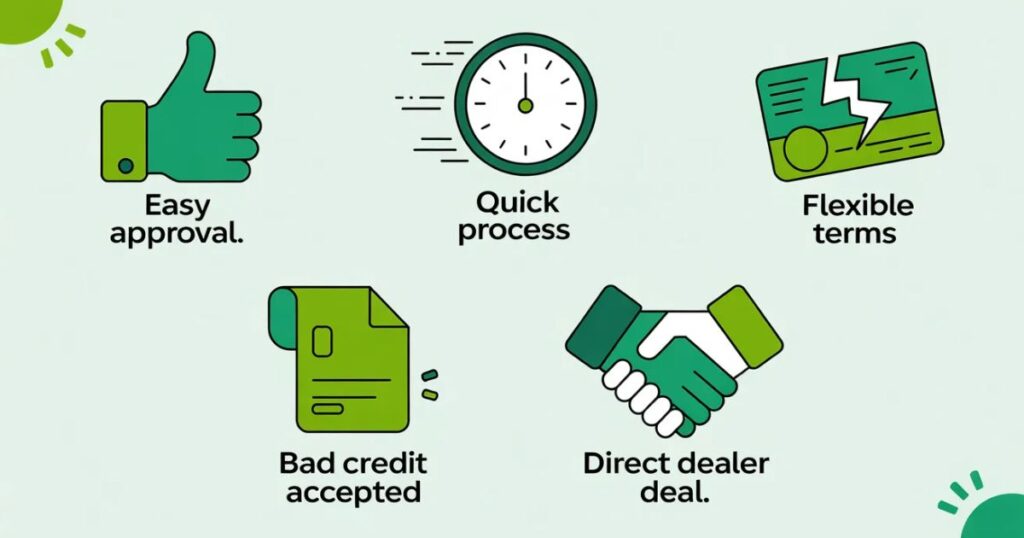

The first and most obvious advantage is sales conversion rate. Removing the upfront cost barrier converts browsers into buyers. A study by Splitit found that 76% of consumers are more likely to complete a purchase when a payment plan is available. That’s not a small bump — that’s a business-changing shift. Customers who might have walked away now say yes on the spot.

| Pro | Business Impact | Who Benefits Most |

|---|---|---|

| Expanded customer base | Reaches buyers banks reject | Auto dealers, furniture stores |

| Higher sales conversion rate | Fewer walkouts, more closed deals | Retail, healthcare |

| Stronger customer retention | Ongoing payment = ongoing relationship | All industries |

| Full control over terms | No lender fees or delays | Small businesses |

| Interest income | Extra revenue on financed amounts | Any business with margins |

| Faster approvals | Same-day decisions possible | High-ticket sales |

| Competitive edge | Stand out from competitors | Crowded local markets |

Customer retention is honestly the underrated gem here. Think about it — when a customer owes you 18 more monthly payments, they’re not going anywhere. They come back. They refer friends. They feel a genuine connection to your business because you trusted them when the bank didn’t. That loyalty is worth far more than any individual sale.

Vendor finance and captive finance programs at larger companies have proven this for decades. Toyota Financial Services, Apple’s installment program, Harley-Davidson’s credit arm — these aren’t side projects. They’re profit engines. Small businesses can build the same engine at a smaller scale, and the profit margin impact is real.

5 Critical Cons of In-House Financing Most Businesses Ignore (Until It’s Too Late)

Nobody likes talking about the downsides. But skipping this part is exactly how businesses end up in trouble six months into a financing program they weren’t ready for.

Loan default risk is the big one. When a customer stops paying, you absorb the loss — not a bank. Not an insurance company. You. The national average default rate for buy-here-pay-here auto dealers sits around 6–8%, according to the National Alliance of Buy Here Pay Here Dealers. In healthcare, it’s closer to 2–3%. Know your industry number before you start.

| Con | Why It Hurts | How Bad It Can Get |

|---|---|---|

| Loan default risk | Lost revenue with no bank backup | 5–10% of portfolio gone annually |

| Admin burden | Collections, tracking, paperwork | Can consume 10+ staff hours/week |

| Regulatory compliance | TILA, state laws, licensing requirements | Fines, lawsuits, license revocation |

| Capital tie-up | Cash locked in receivables | Cash flow crisis in slow months |

| Credit assessment difficulty | Bad vetting = high defaults | Cascading losses if ignored |

Cash flow management is where things get quietly painful. You sell a $5,000 item but collect $200/month. Meanwhile you need to restock inventory, pay staff, and cover rent. That gap between what you sold and what you’ve collected is real and it compounds fast if you’re not watching it carefully.

Regulatory issues are the con that genuinely scares finance attorneys. The Truth in Lending Act (TILA) requires you to disclose APR, total finance charges, and payment schedules in very specific ways. Miss a disclosure and you’re legally exposed. Some states require a lending license just to offer installment plans to customers. This isn’t optional fine print — it’s federal law.

In-House Financing Pros and Cons by Industry: Retail, Auto, Healthcare & Home Improvement

The experience of offering in-house financing is completely different depending on your industry. What works beautifully for an auto dealer can be a compliance nightmare for a healthcare provider. Context shapes everything here.

Auto dealerships — especially buy-here-pay-here lots — built their entire business model around in-house financing. The average deal size runs $8,000–$25,000, which justifies the admin overhead. The biggest challenge is repossession. When customers default on a vehicle, recovering and reselling it costs time, money, and sometimes legal fees. Still, BHPH dealers consistently report net profit margins of 18–22% when they manage credit risk management tightly.

| Industry | Average Deal Size | Default Rate | Top Compliance Concern |

|---|---|---|---|

| Auto (BHPH) | $8,000–$25,000 | 6–8% | State lending laws, repossession rules |

| Retail | $200–$2,000 | 3–5% | TILA disclosure requirements |

| Healthcare/Dental | $500–$15,000 | 2–3% | HIPAA + TILA overlap |

| Home Improvement | $3,000–$50,000 | 4–6% | Contractor lien laws, long repayment terms |

Retail in-house financing — think furniture, electronics, jewelry — works well when ticket prices are high enough to justify the program’s overhead. A $300 sofa with 12 monthly payments isn’t worth the paperwork. A $2,500 bedroom set absolutely is. The math has to make sense before you build the infrastructure.

Healthcare is a uniquely sensitive sector. Patients financing elective dental work or cosmetic procedures often have mixed feelings about monthly payments — they want the treatment but feel awkward discussing money with a provider they trust for health decisions. Practices that handle this with care and transparency see exceptional customer retention and dramatically lower abandonment rates on treatment plans.

How In-House Financing Pros and Cons Differ for Small vs. Large Businesses

Scale changes everything. A national retailer and a neighborhood appliance shop are playing completely different games — even if they’re offering the same type of payment plan.

Small businesses feel default losses personally. One customer who stops paying a $4,000 balance isn’t a rounding error — it’s a real hit. Large businesses build default rates into their financial models and absorb losses across thousands of accounts. Cash flow management at a small business level demands much tighter controls and faster response times when payments go late.

| Factor | Small Business | Large Business |

|---|---|---|

| Capital reserves | Thin — defaults hurt immediately | Deeper — losses absorbed across portfolio |

| Admin capacity | Often owner-managed | Dedicated finance teams |

| Regulatory compliance | High risk without legal support | In-house legal and compliance departments |

| Customer relationship | Personal and trust-based | Transactional |

| Technology access | Requires affordable tools | Enterprise loan management system |

| Default recovery | Difficult, often written off | Structured collections process |

Here’s what most small business guides miss: the personal customer relationship is actually a competitive advantage in in-house financing. When a small business owner knows their customer by name, they can have a real conversation when payments get tight. That conversation prevents defaults far more effectively than an automated collections call. Large businesses can’t replicate that human touch — and it shows in their numbers.

In-House Financing vs. Third-Party Lenders: Which Model Wins in 2025?

Third-party lenders like Synchrony, Affirm, CareCredit, and GreenSky offer a tempting deal: let them handle the financing, you just sell. No default risk. No compliance headaches. Sounds great — until you look at what you’re actually giving up.

Merchant fees from third-party lender programs typically run 2–8% of the financed amount. On a $10,000 sale, that’s up to $800 gone before you’ve covered a single operating expense. More importantly, the customer relationship now belongs to the lender. They get the payment data, the contact history, and the marketing opportunity. You get one transaction.

| Criteria | In-House Financing | Third-Party Lender |

|---|---|---|

| Approval speed | Same-day, on-site | 1–3 business days |

| Customer relationship | You own it | Lender owns it |

| Interest revenue | Stays with you | Goes to lender |

| Loan default risk | Your responsibility | Lender absorbs it |

| Regulatory compliance | Your burden | Lender’s burden |

| Upfront cost | Software + staff time | Merchant fees (2–8%) |

| Term flexibility | Fully customizable | Standardized products |

Flexible payment options are genuinely better when you control them. You can offer a 0% introductory period, adjust payment dates for good customers, or restructure terms when someone hits a hard month. A third-party lender follows their script — not yours.

That said, third-party models make sense for high-volume, lower-margin businesses that can’t absorb default risk. The answer isn’t always in-house financing. But if your margins support it and your customer base is relationship-driven, keeping the financing in-house almost always wins long-term.

Is In-House Financing Worth the Risk? A Real Cost-Benefit Breakdown

Let’s get specific. Abstract discussions about risk and reward are fine — but real numbers tell a cleaner story. Here’s what a mid-sized American retailer with $500,000 in annual financed sales might actually experience.

| Item | Annual Cost | Annual Benefit |

|---|---|---|

| Loan management software | $3,600 | — |

| Staff time (5 hrs/week @ $30/hr) | $7,800 | — |

| Legal/compliance counsel | $4,000 | — |

| Default losses (est. 4%) | $20,000 | — |

| Interest income (12% APR avg.) | — | $32,000 |

| Increased sales volume (15% lift) | — | $75,000 |

| Repeat customer revenue | — | $20,000 |

| Estimated Net Benefit | $35,400 | $127,000 |

Net positive: approximately $91,600 annually. That’s not hypothetical — that’s a realistic scenario for a business that manages its program properly. The profit margin impact is meaningful, especially when compounded over several years.

Businesses that skip the discipline — no income verification, no written contracts, no collections process — flip those numbers fast. The default losses climb. The interest income shrinks. The legal exposure grows. The math only works when you run the program like a real financial product, because that’s exactly what it is.

Who Should Offer In-House Financing? Key Pros, Cons, and Qualification Criteria

Not every business is ready for this. Honestly, jumping in too early is one of the most common and costly mistakes owners make. The enthusiasm is understandable — the upside is real. But so is the downside when you’re not prepared.

Here’s a clean qualification framework. If you check five or more of these boxes, you’re likely ready to launch. Fewer than three, and you need to shore up your foundation first.

| Criteria | Ready ✅ | Not Ready ❌ |

|---|---|---|

| Average transaction value | Above $500 | Below $200 |

| Customer repeat rate | High | Mostly one-time buyers |

| Cash reserves | 3–6 months operating capital | Tight month-to-month |

| Staff capacity | Admin time available | Already stretched |

| Legal access | Compliance counsel available | No legal support |

| Industry default rate | Below 5% | Above 10% |

| Customer credit profile | Mixed (some subprime okay) | Predominantly deep subprime |

Bad credit financing readiness deserves its own mention. Serving subprime customers is possible and profitable — but only if you have the vetting process and collections infrastructure in place before you start. Starting with a subprime -heavy customer base and no experience is a fast track to high defaults.

Start with a pilot. Finance 20–30 transactions. Track every payment. See how your customers behave before you scale the program. The businesses that build confidently are the ones that tested carefully first.

In-House Financing Pros and Cons for Bad Credit Customers: What Sellers Must Know

Over 34% of American adults carry a credit score below 670, according to Experian’s 2024 State of Credit report. That’s roughly 88 million people who face automatic rejection from traditional lenders. For businesses willing to serve them fairly, that’s an enormous market.

Bad credit financing works when you shift your approval criteria. Instead of relying on credit scores alone, focus on income verification, employment stability, and debt-to-income ratio. A customer with a 580 credit score and a steady $55,000 income is often a safer bet than someone with a 650 score and five maxed-out credit cards. The score tells part of the story — not all of it.

| Factor | Why It Matters for Bad Credit Customers |

|---|---|

| Income verification | Proves ability to repay regardless of past history |

| Down payment (10–30%) | Reduces your exposure and increases buyer commitment |

| Employment stability | 6+ months at same job signals reliability |

| Debt-to-income ratio | Should stay below 40% including new payment |

| References | Personal or professional references add context |

Here’s something nobody talks about enough: bad credit customers who get approved are intensely loyal. They remember who said yes when everyone else said no. That emotional connection drives referrals, repeat purchases, and on-time payments at rates that often surprise first-time in-house lenders. Treat them with respect and structure their terms fairly — not predatorily — and they’ll reward you for it.

Always consult your state’s usury laws before setting interest rates. The Consumer Financial Protection Bureau maintains updated state-by-state guidance on lending rate caps. Charging above legal limits, even accidentally, creates serious liability.

Top Red Flags in In-House Financing and How Smart Businesses Overcome Them

Every financing program eventually shows stress. The smart move isn’t pretending problems won’t happen — it’s knowing what warning signs to watch for and acting fast when they appear.

A default rate above 8% is the clearest red flag. It means your vetting process is too loose. Either you’re approving customers without proper income verification or you’re ignoring debt collection signals until accounts are already far past due. Fix this by tightening your approval criteria and implementing a 3-day late payment follow-up protocol — not a 30-day one.

| Red Flag | Root Cause | Fix |

|---|---|---|

| Default rate above 8% | Weak customer vetting | Strengthen income and DTI verification |

| Collections consuming staff time | No automated follow-up | Implement loan management system |

| Customers constantly requesting restructuring | Terms too aggressive originally | Extend repayment windows upfront |

| Legal disputes or complaints | Regulatory compliance gaps | Hire consumer lending attorney immediately |

| Persistent cash flow tightness | Too much capital in receivables | Raise minimum down payment requirement |

| No written contracts | Massive legal exposure | Standardize all agreements immediately |

KYC AML compliance — Know Your Customer and Anti-Money Laundering protocols — aren’t just for banks. Any business offering installment credit above certain thresholds may have KYC obligations under state and federal law. This is genuinely underappreciated in small business circles. A quick consultation with a financial compliance attorney costs a few hundred dollars. A regulatory fine costs infinitely more.

Build a monthly portfolio review into your operations. Thirty minutes reviewing which accounts are current, which are 30 days late, and which are trending toward default saves thousands in recovery costs later.

In-House Financing Pros and Cons: Cash Flow, Default Risk, and Compliance Explained

Cash flow management is the silent killer of in-house financing programs. You can have a profitable portfolio on paper and still run out of operating cash if too much of your revenue is locked in future receivables. This is not theoretical — it’s one of the most common reasons small business financing programs collapse.

The standard recommendation from small business financial advisors is to keep your financed receivables portfolio below 40% of total monthly revenue. Above that threshold, a spike in defaults or a slow sales month can create a genuine cash crisis. Building a default reserve fund — typically 3–5% of your total financed portfolio — before you start is non-negotiable if you’re serious about this.

Loan default risk varies sharply by industry. Healthcare practices consistently report the lowest default rates because patients have an emotional and physical stake in their treatment outcomes. Buy-here-pay-here auto dealers see the highest rates because their customer base is predominantly subprime. Knowing where your industry sits helps you calibrate reserve requirements and approval thresholds from day one.

On compliance: the Truth in Lending Act (TILA) is federal law. It requires you to clearly disclose the APR, total finance charge, total amount financed, and total payment amount in every consumer credit agreement. Regulatory compliance also includes state-specific requirements — some states require a lending license even for simple installment plans. The CFPB’s compliance resources page is genuinely useful and free. Use it before you draft a single contract.

Automated underwriting tools have made compliance significantly easier. Modern loan management systems flag missing disclosures, calculate APR automatically, and generate compliant contracts. This removes the human error that creates most compliance violations.

How to Maximize the Pros and Minimize the Cons of In-House Financing with Technology

Technology changed this game completely. Five years ago, running an in-house financing program meant spreadsheets, manila folders, and a lot of stressed phone calls chasing late payments. Today, loan management system platforms do the heavy lifting at a fraction of the cost of a part-time employee.

Automated underwriting is probably the highest-impact improvement available to small businesses right now. Instead of manually reviewing each application, automated systems evaluate income, employment, and debt-to-income ratios in minutes. They generate approval decisions, flag high-risk applications, and produce compliant contracts automatically. That’s not just efficiency — it’s consistency, which is exactly what regulators want to see.

| Platform | Best For | Approximate Monthly Cost |

|---|---|---|

| LoanPro | Full loan lifecycle management | $249+/month |

| Collect! Debt | Debt collection automation | $99–$399/month |

| TimePay | Auto dealer financing | $149–$299/month |

| Lendio | Small business loan origination | Free (commission-based) |

| QuickBooks + add-ons | Basic receivables tracking | $30–$90/month |

Automated payment reminders reduce late payments by up to 35%, according to data from loan servicing platform LoanPro. That’s not a trivial improvement. A 35% reduction in late payments directly lowers your default rate, reduces staff time on collections calls, and improves cash flow management across the board.

KYC AML compliance tools integrated into modern financing platforms also protect businesses from unknowingly financing fraudulent transactions. Identity verification, document scanning, and watchlist screening used to require dedicated compliance staff. Now they’re built into software that costs less than $300 a month.

Here’s the honest bottom line on in-house financing pros and cons: the program itself isn’t the risk. Running it without systems, processes, and proper legal grounding is the risk. Businesses that invest in the right tools from the start consistently outperform those that try to manage it manually — and they sleep better at night knowing their compliance bases are covered.

The opportunity is genuinely significant. American consumers want flexible payment options more than ever. They want to buy from businesses that trust them. If you can build a program that serves those customers well, manages risk intelligently, and stays on the right side of the law, you’re not just offering financing — you’re building a lasting competitive advantage that your competitors without a financing program simply can’t match.

Frequently Asked Questions

What is in-house financing? In-house financing means the business itself acts as the lender, offering customers the ability to pay for goods or services in installments — without involving a bank or third-party lender.

How does in-house financing work? The business sets the credit terms, collects payments directly, and absorbs the default risk. Customers make monthly payments to the business instead of to a financial institution.

Is in-house financing a good idea? It depends on your margins, customer base, and operational capacity. For businesses with high-ticket items and a loyal customer base, it can meaningfully increase revenue and customer retention.

Should I offer in-house financing? If your average transaction exceeds $500, your cash reserves can absorb 3–5% default losses, and you have access to compliance guidance, you’re likely a strong candidate.

What are the risks of in-house financing? The primary risks are loan default risk, cash flow strain from tied-up receivables, and regulatory compliance violations under TILA and state lending laws.

What happens if a customer defaults? You absorb the loss. This is why default reserve funds and tight vetting processes are essential. Debt collection procedures should be established before you launch.

Can bad credit customers get in-house financing? Yes — and they often make excellent customers. Focus on income verification and employment stability rather than credit score alone.

What is the difference between in-house and third-party financing? With in-house financing you control the terms and keep the interest income but carry the default risk. With a third-party lender, they carry the risk but charge merchant fees of 2–8%.

What licenses do I need for in-house financing? It varies by state. Many states require a lending license for consumer installment credit. Check your state’s financial regulation authority or consult the CFPB’s guidance.

How to reduce risk in in-house financing? Use income verification, require meaningful down payments, implement a loan management system, build a default reserve fund, and maintain full regulatory compliance from day one.

Is in-house financing worth it for small businesses? For the right business, absolutely. The key is building the program on solid infrastructure — not launching fast and fixing problems later.

Ideas to Help You Think Smarter About Money.